DailyReport - test area

+++ Market assessment in the morning +++

The DailyReport is cancelled in week 32 due to vacation.

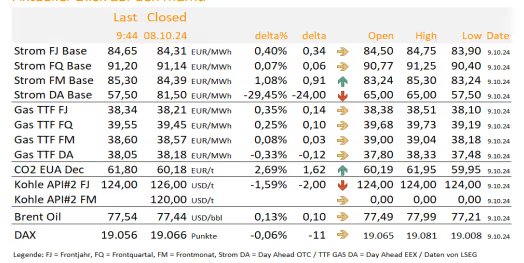

| Instrument | Last | delta% | delta | Open | High | Low | Date | ||

|---|---|---|---|---|---|---|---|---|---|

| 17:59 | 16.10.24 | Change | |||||||

| Strom FJ Base | 86,85 | 86,75 | 0,12% | ▲ | 0,10 | 87,12 | 87,40 | 86,40 | 17.10.24 |

| Strom FQ Base | 94,55 | 94,26 | 0,31% | ▲ | 0,29 | 95,16 | 94,20 | 17.10.24 | |

| Strom FM Base | 86,18 | 87,51 | 0,74% | ▲ | 0,65 | 87,26 | 89,28 | 87,26 | 17.10.24 |

| Strom DA Base | 104,30 | 70,50 | 47,94% | ▲ | 33,80 | 104,00 | 104,30 | 104,00 | 17.10.24 |

Market outlook from 30.10.2024

Current look at the market

Uncertainty persists - Still waiting for Israel's response

Heading 1

Heading 2

Heading 3

Heading 4

Heading 5

Heading 6

Lorem ipsum dolor sit amet, consectetur adipiscing elit, sed do eiusmod tempor incididunt ut labore et dolore magna aliqua. Ut enim ad minim veniam, quis nostrud exercitation ullamco laboris nisi ut aliquip ex ea commodo consequat. Duis aute irure dolor in reprehenderit in voluptate velit esse cillum dolore eu fugiat nulla pariatur.

Block quote

Ordered list

- Item 1

- Item 2

- Item 3

Unordered list

- Item A

- Item B

- Item C

Bold text

Emphasis

Superscript

Subscript

Chinese stock market disappointed by economic measures (CSI 300 index, daily chart)

source: LSEG

Dennis Warschewitz

Stefan Küster

Tobias Waniek

research@enerchase.de

Marktausblick vom 09.10.2024

Current look at the market

Uncertainty persists - Still waiting for Israel's response

Heading 1

Heading 2

Heading 3

Heading 4

Heading 5

Heading 6

Lorem ipsum dolor sit amet, consectetur adipiscing elit, sed do eiusmod tempor incididunt ut labore et dolore magna aliqua. Ut enim ad minim veniam, quis nostrud exercitation ullamco laboris nisi ut aliquip ex ea commodo consequat. Duis aute irure dolor in reprehenderit in voluptate velit esse cillum dolore eu fugiat nulla pariatur.

Block quote

Ordered list

- Item 1

- Item 2

- Item 3

Unordered list

- Item A

- Item B

- Item C

Bold text

Emphasis

Superscript

Subscript

Chinese stock market disappointed by economic measures (CSI 300 index, daily chart)

source: LSEG

Dennis Warschewitz

Stefan Küster

Tobias Waniek

research@enerchase.de

Market review of 08.10.2024

Heading 1

Heading 2

Heading 3

Heading 4

Heading 5

Heading 6

Lorem ipsum dolor sit amet, consectetur adipiscing elit, sed do eiusmod tempor incididunt ut labore et dolore magna aliqua. Ut enim ad minim veniam, quis nostrud exercitation ullamco laboris nisi ut aliquip ex ea commodo consequat. Duis aute irure dolor in reprehenderit in voluptate velit esse cillum dolore eu fugiat nulla pariatur.

Block quote

Ordered list

- Item 1

- Item 2

- Item 3

Unordered list

- Item A

- Item B

- Item C

Bold text

Emphasis

Superscript

Subscript